CHARTS: Iron ore, copper price – shot… chaser

Investment bank BMO Capital Markets this week made some changes to its metals and mining outlook for the second half of the year, raising expectations pretty much across the board.

BMO raised its H2-2021 estimates for most base metals with nickel, aluminum, zinc and lead forecasts adjusted upwards by 7– 8%.

Cobalt prices are expected to end the year higher on the back of a strong cyclical and structural demand outlook, and the bank has also become more bullish on nickel, now expecting a deficit in 2021 vs its expectations of a 100kt surplus prior.

Even iron ore prices – which have been defying gravity above $200 a tonne this year – were upgraded. BMO pared back the pace of its forecasted decline for the steelmaking raw material and also gave hard coking coal a big bump, raising its forecast by 14%.

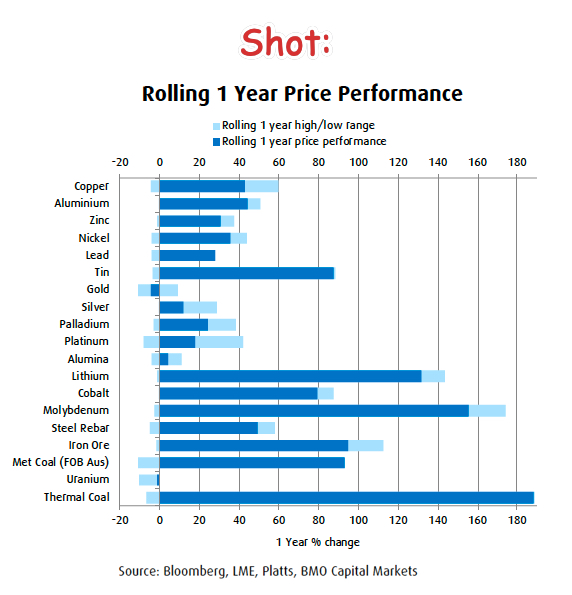

So far so good. With prices for all commodities running hard over the past year – figure 1 – some moderation over the rest of the year is to be expected:

“With global industrial production growth rates now having peaked, across industrial metals the focus across base metals and bulk commodities is now shifting towards duration of prices being maintained at current elevated levels. Demand momentum is starting to wane, which is the dominant factor behind expected declines from spot prices by year-end. However, across supply chains a combination of pandemic-related issues and logistical constraints means that replenishing inventories at end users is set to take longer.”

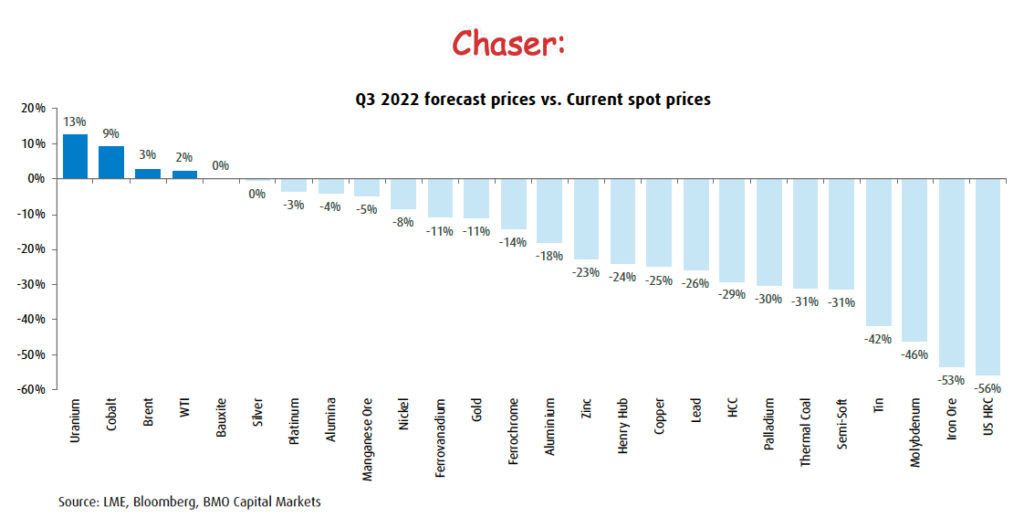

But comparing today’s prices with BMO’s forecasts just a short year from now is, in a word, sobering.

More News

Vale chairman Stieler pushed out by pension fund

July 06, 2026 | 04:40 pm

South32’s Arizona $2 billion zinc and manganese mine to get US approval

July 06, 2026 | 04:22 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments