China-backed JV set to start work at Simandou

China is close to granting approval to some of its biggest state-owned companies to start developing the northern area of Simandou in Guinea, one of the world’s largest untapped iron ore deposits, sources familiar with the process said on Thursday.

A joint venture between Guinea’s Société Miniere de Boke (SMB) and Singapore’s Winning International Group, whose investors include Chinese aluminium producer Shandong Weiqiao and the Yantaï Port Group, secured in November rights to an area of the massive iron deposit, under Guinea’s mountainous jungle.

But the partners have been unable to proceed as they need the official go-ahead from China’s State-owned Assets Supervision and Administration Commission (SASAC), which oversees the largest government-owned enterprises.

The prospect of seeing Simandou coming online within five years is seen as a threat by the world’s top iron ore producers

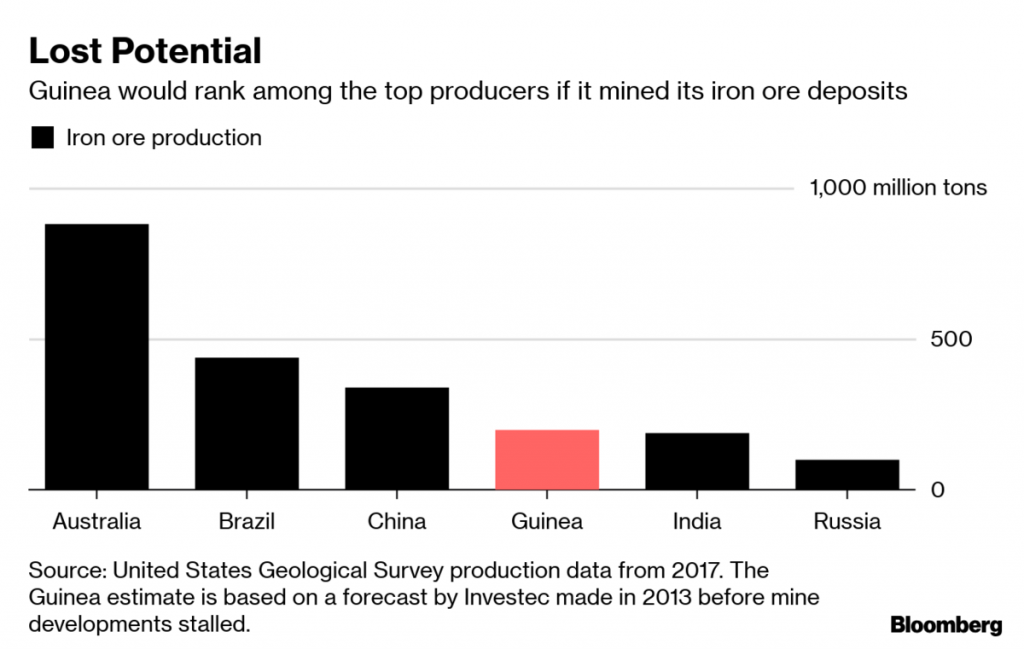

For over a decade, it seemed that Guinea’s crown jewel deposit would never be mined, as it was caught up in wrangles between companies that held rights to it and authorities in the West African nation.

In 2008, one of Guinea’s former dictators stripped Rio Tinto’s rights over two of the four blocks the deposit had been divided on and handed them to Israeli billionaire Benny Steinmetz’s BSG Resources (BSGR).

The world’s No. 2 miner was able keep the two southern blocks, but only after paying $700 million to the government in 2011. That guaranteed Rio tenure for the lifetime of the Simandou mine.

That deal came under scrutiny in 2016, forcing the company to fire two senior managers over a questionable $10.5 million payment made to a consultant who helped the company secure the two blocks and alerted authorities, including the US Department of Justice and the UK’s Serious Fraud Office.

Several investigations over bribery and corruption followed, until a settlement between Steinmetz and Guinea was reached early last year, ending the bitter and long-dragged out dispute involving Rio Tinto, Vale SA and BSGR.

As part of the agreement, Steinmetz’s company agreed to walk away from the asset, but retained the right to mine the smaller Zogota deposit.

Major new source

The prospect of seeing Simandou coming online within five years is seen as a threat by the world’s top producers of the steelmaking material. The deposit is not just massive — it holds two billion tonnes of iron ore — but the quality the expected output will have some the highest grades in the industry.

China is actively pushing forward with the project and a decision should come soon as SASAC is fine-tuning details, including how the project will be funded, the sources said.

Chinalco will be involved in the development, but SASAC is also reaching out to other state-owned companies about building a port and a 650-kilometer (400-mile) railway.

Rio Tinto holds a 45% stake in blocks three and four of Simandou, which it is actively planning to develop. State-controlled Chinalco owns 40% and the Guinea government 15%.

Both companies are said to be trying to persuade authorities to let them use ArcelorMittal’s railway to a port in neighbouring Liberia.

China’s resource dependence on Guinea has increased in recent years. In 2017, Beijing agreed to loan President Condé’s administration $20 billion over almost 20 years in exchange for bauxite concessions.

Analysts say Guinea’s population has so far seen little benefit from Chinese investment.

(With files from Bloomberg)

More News

Boliden in talks to buy Votorantim’s controlling stake in Nexa

Nexa is one of the world's leading zinc producers.

July 02, 2026 | 02:50 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments