Even the iron ore price will bottom

Iron ore fell to a record low on a spot price basis this week stopping just short of a crash through $40 a tonne. The price dropped 47% during 2014 and declines so far this year come to more than 40%. Today’s price compare to $190 a tonne hit February 2011 and an average of $135 a tonne in 2013.

For an iron ore price below $40 you have to go back to 2007 when annual contract pricing between the Big 3 producers – Vale, Rio Tinto and BHP Billiton – and Chinese and Japanese steelmakers were still the industry norm.

During the 2008 negotiations, the so-called benchmark was upped 68% to $60.80, but the triumvirate continued to lose out on billions under annual contract pricing. Growing Chinese port stockpiles saw action in the industry shift to mills and traders, ushering in the era of rapidly rising and volatile prices based on spot assessments by MetalBulletin and The Steelindex.

The big three producers – Vale, Rio Tinto and BHP Billiton – have been following a scorched earth strategy of raising output and slashing costs to weather low prices and push out competitors.

It’s been highly successful. Up to a point.

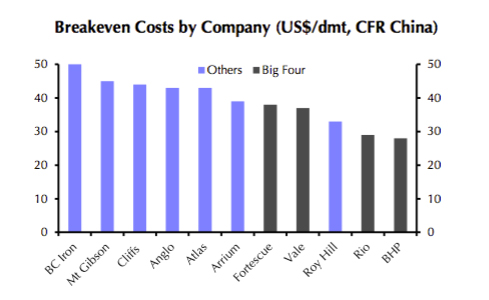

On cash costs basis major producers have been adding capacity in the teens, but breakeven costs including freight, insurance and other costs range between $28 – $39.

The Big 3 (and no 4 Fortescue) have all vowed to cut mining costs even further with Vale boasting recently that it’s 90mtpa S11D project in the Amazon will push costs into single digits.

But these cost savings have been largely thanks to a falling currency with the real dropping to record lows this year. A weaker Aussie dollar has also helped Pilbara producers as has falling diesel prices.

Freight rates for Capesize vessels (named so because the ships are too wide for the Panama canal), the predominant carrier used in the 1.3 billion tonnes seaborne iron ore trade fell to just $4,015 a day last week (it topped out a ludicrous $234,000 in June 2008).

But like currencies and crude oil, freight rates can’t decline indefinitely.

Capital Economics, a London-headquartered independent researcher, in a note on Friday says that while the price of iron ore may fall below $40 a tonne as more low cost supply (notably S11D and 50mtpa Roy Hill in Australia) is added, it won’t stay there for long.

Senior commodities economist John Kovacs says the fact that prices are now approaching the breakeven cost for even the largest miners, coupled with a modest rise in global iron ore demand next year and near term supply losses (BHP-Vale joint venture Samarco will take 9mt off the market and more Chinese mines will close) could spell a gradual recovery.

The closure of high-cost capacity will increase the market power of the larger miners and could provide the impetus for prices to rise argues Kovacs.

Capital Economics sees the price of the steelmaking raw material to rise steadily, reaching $55 a tonne by the end of 2016.

Source: Capital Economics, UBS, Bloomberg

Image of ice fishing on the Hai river in Tianjin by galexkeene on Flickr

More News

BHP seeks to restart Cerro Colorado mine with $1.5B investment

The copper mine has been closed since late 2023 after it was denied its water permit.

July 02, 2026 | 10:43 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

3 Comments

PaoloUSA

For once the mambo jambo of 20 USD/t cash cost is not brought up. Finally the beginning of the recognition that it was simply a shot in the foot with the condiment of some form of hubristic approach that made some of the biggies believe they could control the market. 1980s unsustainable business model at its best!

marpy

To this point, the shareholders of the big 3 had been willing to let management play its game of increasing production with the goal of maximizing market share and hence profitability when the market turned. This it seems is rapidly changing as profitability and share prices tank and the end game seems even further away. When I look at the big 3, Rio Tinto is in perhaps the best shape followed by BHP and way further behind, Vale which has high debit and has always it seems been dogged by corruption and political interference. I suspect that share holder pressure and the reality that the demand is not coming back as quick as management expected will force a change it strategy. Having said this, by the time we see a change the goal of maintaining market share will be largely fulfilled as a slow rise from $40 will still put many high cost suppliers out of business. Note that the big 3 can increase profit margins while keeping the price of ore low just buy shutting down their own higher cost production as lower cost production comes on line. Perhaps this is their game plan for dealing with the reduced demand while still meeting their goals.

JMO

PaoloUSA

BHP declared cash cost in the FY 2015 is 19$/t (31% reduction from FY2014), despite this their Underline EBIT was 6.9 bil $ against a FY 2014 value of 12.1 bil $ (46% decline)………….so much for the cash cost mambo-jambo.

Interesting is that their average declared realized price for iron ore was 61$/wmt FOB Australia over FY2015 and yet the EBIT is in free fall.

If the marker stabilizes at low forties for another year, they will sink like anyone else, not considering the impairments in the oil sector.

To note that of their combined production 77% is fines of 57% to 62.5%Fe grade, only 23% is lumps, a more sustainable product given the China drive for a greener steel industry. Not a great set of ingredients for a sustainable future. As usual a lot of “food for investors”.