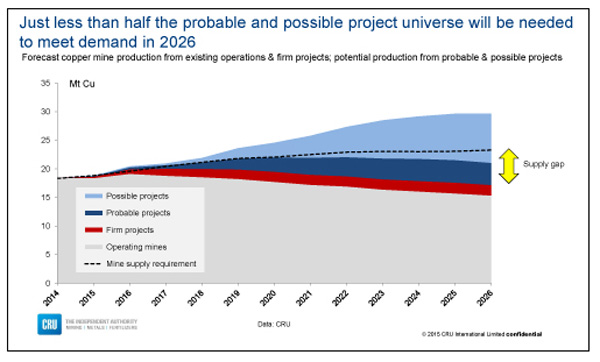

Less than half of copper projects needed to meet demand

Las Bambas: 460,000 tonnes per year starting early 2016. Image: MMG

Copper is down 9.7% compared to a year ago, but has recovered well from five-and-half-year lows struck in January. Most analysts expect copper to move into a surplus in excess of 200,000 tonnes this year after a mostly balanced 2014, but the copper industry has a long history of supply disruptions.

Typical disruptions associated with adverse weather (top producer Chile has swung from severe drought to worst floods in 80 years in 2015), technical problems, power shortages or labour activity coupled with falling grades and dirty concentrates at old mines make forecasting a tough proposition.

To these variables add more recent factors affecting future supply which includes the weak price which makes it difficult for miners to raise development finance (or raise wages for that matter). That leads to project deferrals, commissioning delays and downsizing of mine plans.

A new report by London-based CRU, an independent mining, metals and fertilizer researcher, estimates that some 200,000 tonnes of potential copper mine output destined for markets this year have been lost due to these factors.

By 2021 that figure would’ve increased to close to 3 million tonnes which compares to global annual production of under 20 million tonnes. At the same time output at existing operations are expected to peak next year and from 2020 a “marked downtrend in committed production will set in” according to Christine Meilton, Principal Consultant at CRU.

All of which should be great news for the copper price. Not so fast says Meilton:

There is no shortage of potential resources available to fill this gap. CRU’s portfolio of projects includes 231 “probable” and “possible” projects with total maximum potential output of 12.9M tonnes, while a further 6.6Mt is potentially available from earlier stage projects, those which CRU categorises as “prospects”. In addition, despite difficult financial conditions, grassroots exploration continues.

As the graph shows that means according to CRU estimates just less than half of the probable and possible projects need to get off the ground to fill the supply gap.

Source: CRU

Click here for more from CRU.

More News

BHP seeks to restart Cerro Colorado mine with $1.5B investment

The copper mine has been closed since late 2023 after it was denied its water permit.

July 02, 2026 | 10:43 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

9 Comments

Juan Anes

how did this person projected demand?

how did this person factored in the projects that will fail to start production?

has this ever happened before? i.e that supply of copper is twice the demand? what is different in the world economy that would allow this prediction to happen?

Mike

The development of greenfield site copper projects has been significantly influenced by increasing “green and red tape” not to mention regional ,state and federal politics. An indication of the time line to progress a copper project at Feasibility Study stage to commercial start up is 7 to 9 years. This is also dependent upon the location, infrastructure requirements and the country of production. Increasing copper deposits are found in countries where sovereign risk cause project funding agencies and Mining Boards to take more time to commit .Another contributor to these time schedules is the fact that higher grade copper deposits are found at greater depths thereby significantly increasing the capital cost intensity of the mining methodologies–shaft dev/underground infrastructure versus open pit mining. Recent examples of such factors include the ongoing debate in Mongolia, where u/g mining is a relatively new challenge and the La Granja project (s) in an experienced copper country like Peru.

Therefore it is considered “healthy” that the chart identifies a robustness of opportunity because less than 20% of these will ever “get off the ground (or under it!)”

KopperKat

But what cost of production is involved with that 50% of companies? I also imagine there is no feasibility study on those “probable and possible” so who really knows?

Mike

Agreed Kopperkat

The niceties and time associated with Pre feasibility and Full Feasibility Study activities tends to get lost at the smaller end of the development market, as they strive to accelerate from explorer to producer.Financial institutions look at producers more favourably than explorers. That’s the incentive!!

Fascinating industry –never fails to disappoint. As Arnold shouts “we’ll be back !!”

.

rayban

Probable and possible ? Is that NI43-101 language . Don’t sound so . 2. The mines at .27 to .39 shall disappear and new ones replace them . 3. There are high grade deposits at surface . 4. Nothing stays the same , prices change , demand changes . 5. Any cheapish metal finds more uses , Copper no diff . 5. A little more depth of analysis would be real nice and good . Lack of caution causes losses and job disruption .

As well , it takes time and money to build a mine of any largish size . It also takes a deposit with a longer LOM . Banks are skittish of short term projects with lack of long term possibilities .

Finally …. Oh LOL …. Low oil and gas prices not last for ever . Copper shall return .

Christine

I’d like to provide some more clarification as this has been taken from a longer piece. Projects are classified as firm/probable/possible/prospect or speculative according to the Gateway definitions. Broadly, probable are at the feasibility study stage and possibles at prefeasibility. And we certainly recognise that a significant proportion of these projects won’t make it to production for a variety of reasons. Out of the total potential production from projects that might make it into production by 2026, around half will be needed to meet demand, ie fill the supply gap between demand and production from existing operations and committed projects (ie those under construction). An important factor determining which projects will be developed is, of course, the copper price. Using our copper mining cost model we have constructed a cost curve of the probable and possible projects to determine the long run marginal cost of filling the supply gap, and hence the long run attractor price for copper. Of course, as Mike points out there are several other factors that could kill a project. Indeed it is unlikely that it will only be projects from this particular portfolio of projects that will fill the gap, but some will be replaced by other projects that are currently at an earlier stage.

Finally, Rayban, there is a lot more depth of analysis in our recently published report, the Long Term Market Outlook for Copper.

MINING.com Editors

Thanks for the clarification Christine. I was wondering if CRU assigns a rough “probability” percentage value on the projects you classify as possible/probable/prospects. I assume projects like Las Bambas is in the firm category, but would Oyu Tolgoi Phase II for instance be a “probable” with a 70% chance of happening for arguments sake – Frik.

golddigger69

About a month ago, the CEO of Rio told the world that it would need 9 Escondias to meet demand (and then they shuttered copper exploration!?). Now we get told that there will be a surplus supply in 10 years time. The truth is no one knows what economic, political and geological factors will intervene.

Projects that require long lead times to development (e.g. copper deposits) will need an exceptionally robust economic analysis to secure funding under these conditions of high uncertainty. This will kill (or more precisely delay) many good, viable properties until the metal price goes to exuberant levels. Every time that happens thought, there is significant social desperation due to the theft of metal from unsecured locations (e.g. powerless, unoccupied houses, etc) which literally sucks the life blood from society.

China appears to have decided to hell with the boom bust cycle and secured a number of assets that it can keep running whilst the rest of the world play games over which project is “viable”. It seems that for at least this metal the world really needs to come up with a better model for funding, or risk paying huge prices for marginal increases in production i.e. an unsustainable circumstance.

peter

try getting a new copper mine up and running these days , it is near impossible as NIMBYism is rampant right around the world , many countries also getting far too greedy in terms of taxing mines with royalties making many of these projects just not worth the capital risk not to mention the wages rising far too quickly in what was once considered the 3rd world ….add it up and the squeeze to higher priced copper seems rather obvious