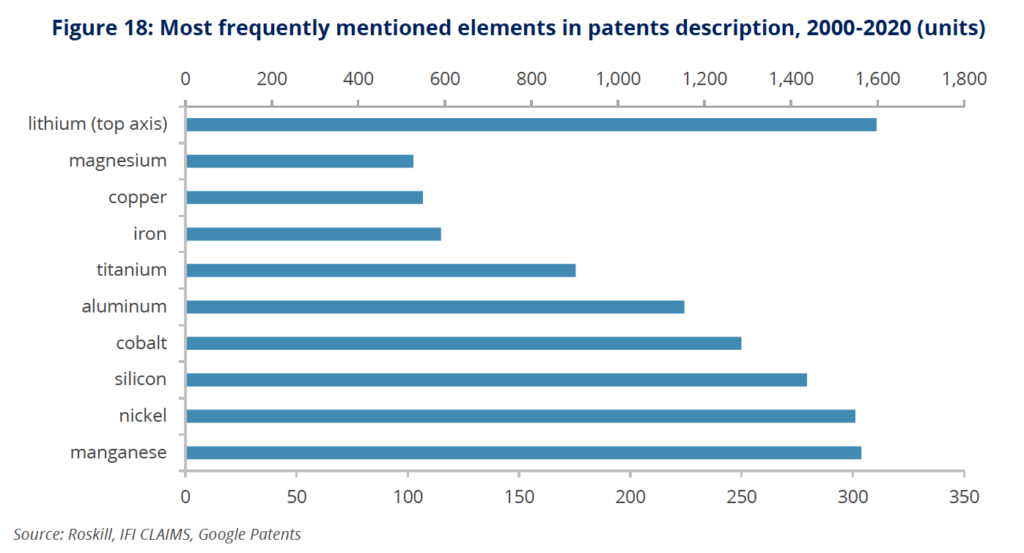

Manganese, nickel, silicon are main focus of battery research

A new whitepaper by Roskill that examines the potential of patent analysis to understand the lithium-ion battery technological landscape found the market trend is decidedly leaning towards nickel, cobalt, manganese and aluminum in terms of material utilization.

Next to these metals is also silicon which, according to Roskill, is gaining share in commercial products and could be considered a technology of ‘today’, rather than ‘tomorrow.’

Manganese, however, is becoming the star of the show, slightly overtaking nickel. The whitepaper points out that this is the result of recent announcements from Tesla and Volkswagen in their battery-related presentations about their interest in Mn-rich chemistries.

“In recent years, lithium-ion batteries, particularly in the EV space, have witnessed some radical changes in different cathode and anode chemistry demand, driven by producers and customers preferences and many market-related factors,” the document reads.

Using a Name Entity Recognition algorithm aimed at mapping the chemical elements in patent descriptions and applying it to the Cooperative Patent Classification (CPC) groups and subgroups to classify battery technology, Roskill experts were able to determine that manganese was mentioned in over 300 patent applications, while nickel was named in close to 300. Silicon was mentioned in about 290, and it was followed by cobalt, which was mentioned in about 250 applications.

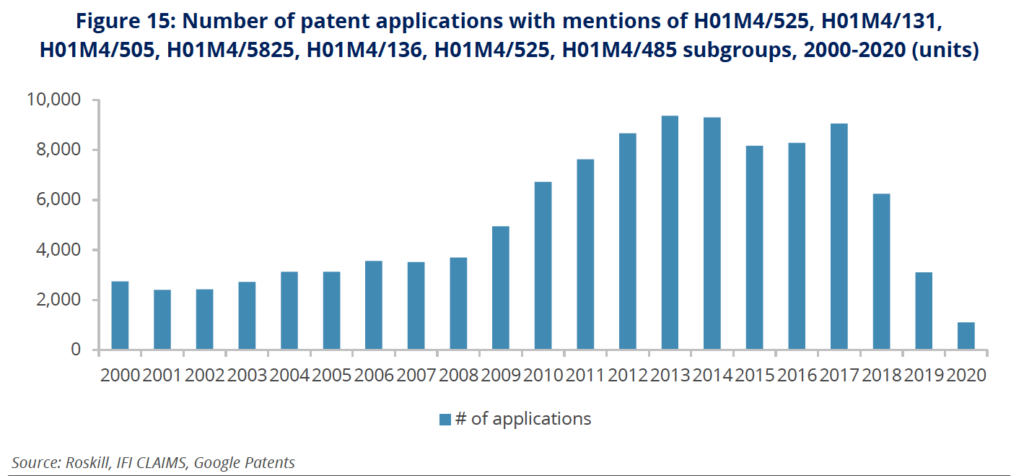

Roskill also reviewed the most popular battery chemistries such as lithium-nickel-cobalt-manganese oxide (NCM), lithium-nickel-cobalt-aluminum oxide (NCA), lithium-iron-phosphate (LFP), lithium cobalt oxide (LCO), lithium-manganese oxide (LMO) and lithium-titanate-oxide (LTO) together, as most frequently CPC groups/subgroups used for its classification overlap.

It found that, in the past five years, 2017 was a peak year with over 8,000 patent applications containing at least one of these chemistries. In 2018, there were 6,000 applications registered, about 5,000 in 2019 and fewer than 2,000 in 2020.

Overall, more than 1.3 million patent records mention a relation to Li-ion batteries and, according to Roskill, the declining trend in 2019-2020 is the result of data availability, rather than an actual representation of ongoing research, as publicly available datasets tend to not be updated frequently.

“Despite this, available data clearly displays tremendous growth in patent applications during the mid-late 2010s,” the report states.

CPC subgroups H01M4/525, H01M4/131, H01M4/505, H01M4/5825, H01M4/136, H01M4/525, H01M4/485.

The analysis also showed that LG and Samsung hold leading positions, with the former connected to almost 7,000 Li-ion chemistry-related patent applications, and the latter with over 4,000.

Both companies had a peak of patent activity in 2012-2014 which, Roskill says, is in line with the general uptake of production and establishing the first large-scale production facilities.

Toyota occupied the third spot in this measure which, in Roskill’s view, makes sense as the Japanese automaker has expressed interest in other electrode research, particularly in solid-state technologies.

Geography: Canada’s potential

Over the past 20 years, the highest patent activity for improvements to, or new battery chemistries was registered in Japan with over 14,000 applications, the US with over 6,700, Korea with over 6,500, and China with about 1,400. However, other countries seem to be emerging and could point to potential growth for battery companies.

“We have already seen a boom of gigafactory announcements in Germany driven by Tesla, CATL and others, but in the top list we also see Canada,” the whitepaper reads. “Canada has a great potential for developing battery production facilities given its resource production capacities. Recently the Canadian government announced plans to build an electric vehicle battery plant.”

What’s next?

“Successful development in the lithium-ion space is at the forefront of many companies including miners, through the supply chain to research institutions and government facilities,” the report reads. “Silicon, lithium-metal anodes and solid-state electrolytes appear to be the next step for the market in the development of battery technologies.”

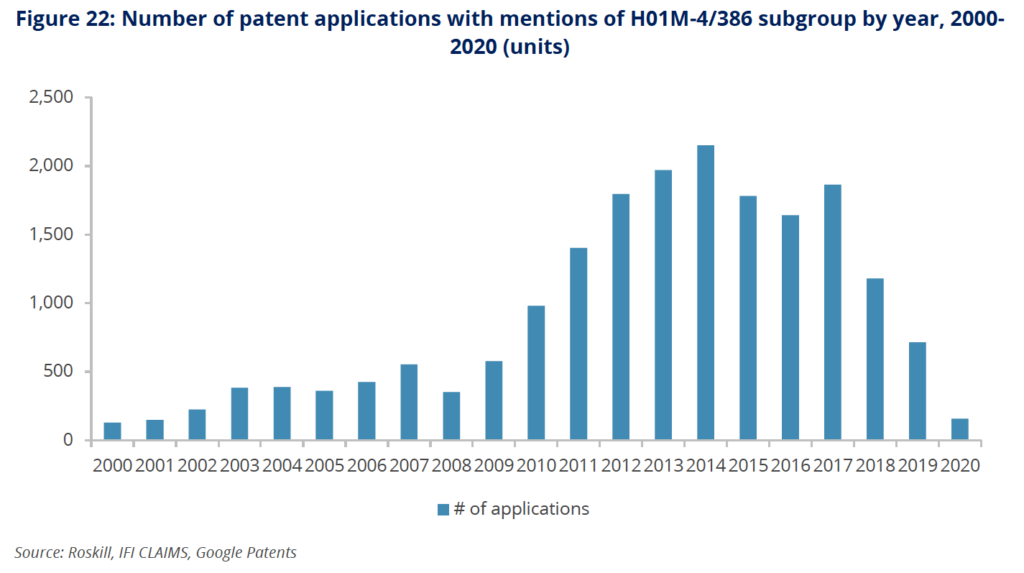

Research on the use of silicon in Li-ion batteries has been happening for a while, with scientists trying to eliminate the possibilities of mechanical damages in cells because of silicon’s swelling during charge-discharge cycles.

In 2014, patents to incorporate silicon in batteries reached a high point at 2,000 submissions, a number that continuously declined thereafter.

“However, research in this direction seems to yield some advances and in 2021 automotive OEMs claim to use silicon-based batteries,” Roskill says. “Among the usual top industry players, we can spot two new names, not mentioned previously – Nexeon and Shin-Etsu Chemical. News that Nexeon acquired important silicon-related patents came out in late 2019. Shin-Etsu Chemical is a major chemical company in Japan producing silicon in various forms, including battery applications.”

When it comes to lithium metal anode applications, the analyst noticed an increase in patent applications from 2010 onwards with a 1,200 submission peak in 2017 and with most activity coming from the biggest producers such as LG, Samsung and Bosch, but with other US-based companies approaching center-stage.

Among those companies are Sion Power, which was founded in 1989 and is currently promoting its own lithium metal battery technology; Eveready, which is a company owned by Energizer Holding and historically was focused on primary cells; and PolyPlus Battery, which is focusing on glass separator in Li-metal batteries and promoting its invention for all major end uses.

In 2014, patents to incorporate silicon in batteries reached a high point at 2,000 submissions

Finally, when it comes to solid-state batteries – which are considered by some as the ‘holy grail’ of the battery industry – 2017 saw a peak with over 4,000 applications, a number that remained steady the following year before showing a decline in 2019 and 2020.

“Solid-state batteries would have higher energy density and solve the biggest problem of using flammable liquid electrolytes,” Roskill says. “Achieving satisfactory conductivity without increased temperature and pressure is the research goal for many companies and institutions.”

Among the top assignees of patents related to solid-state batteries, Toyota is leading with almost 4,500 applications between 2000 and 2020.

“The company announced its commitment to electrification later than others, though was the first among major auto producers thinking about commercialization of solid-state technology. We will need a closer look when it happens, but from the current perspective, Toyota appears to have a competitive advantage in the field of solid-state batteries,” the review states.

Behind the Japanese giant are Panasonic, Samsung and Hyundai with about 1,000 patents each.

More News

Northern Star replaces CEO, activist investor Elliott wants more

July 01, 2026 | 08:29 pm

Ukraine urges swift publication of Irish investigation into alumina exports

July 01, 2026 | 01:22 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

2 Comments

taapo bvirakare

Well written.

Kindly requesting for a copy of the white paper by Roskill.

Regards,

Amanda Stutt

Thank you Taapo, the hyperlink to the report is in the first sentence.