Rare earth supply crunch triggers global power shift: Report

A surge in new rare earth production expected this decade will still fall short of growing global demand, potentially leading to supply gaps and boosting pricing leverage for China — the dominant supplier — as well as the limited number of producers operating outside the country, Bloomberg Intelligence said in a new report.

Governments and industry are scrambling to loosen China’s grip on rare earths, but new supply will arrive too slowly to prevent shortages, shifting pricing power to a handful of miners outside the country, a new report warns.

Geopolitical tensions and export threats have accelerated efforts to diversify supply chains for the critical minerals used in electric motors, electronics and advanced weapons systems, according to BI analysts Jack Baxter and Richard Bourke.

The report, published Monday, expects demand for key rare earth elements to climb about 7% annually through 2030, fueled by growth in electric-vehicle motors, consumer electronics and military uses.

Even as public and private producers prepare to attract about $10 billion in funding in 2026 through capital injections, improved mine economics and fast-tracked permitting, new output will not ease tight market conditions before the end of the decade.

China to lose ground

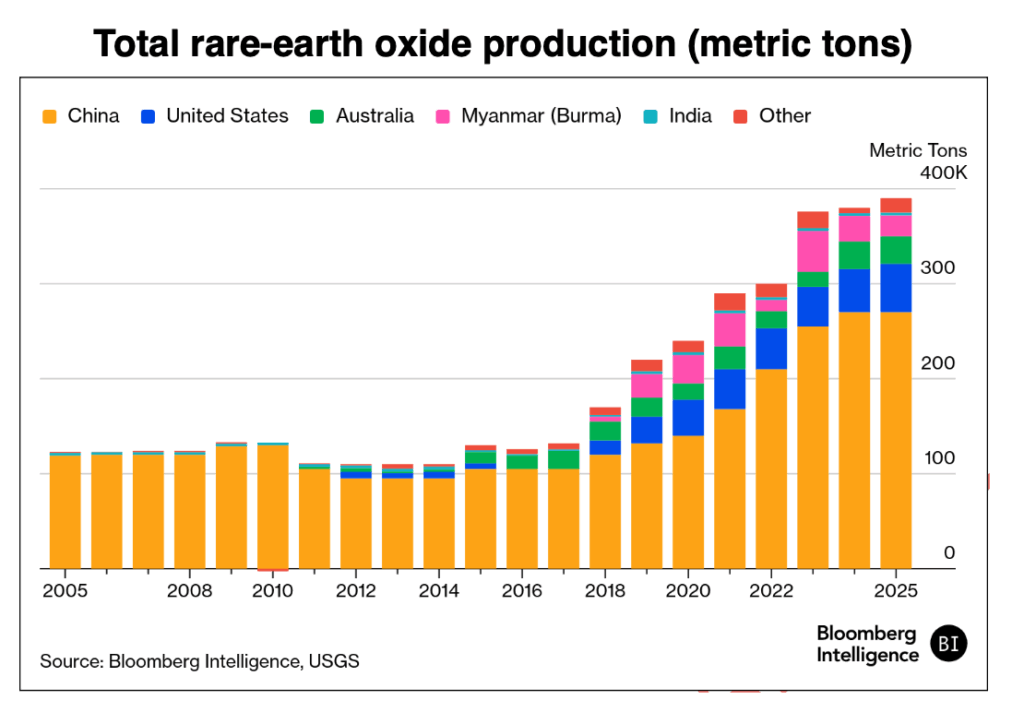

China continues to dominate the sector, accounting for about 90% of rare-earth market value in 2024. But the report predicts that China’s dominance over the rare earths industry will slip by 2030. Rising output elsewhere is expected to cut the Asian giant’s share by 21 percentage points to 69% by then, but supply gaps will persist. That imbalance is set to fracture what was once a globalized market and drive the emergence of regional pricing benchmarks, particularly as import tariffs and other trade barriers take hold.

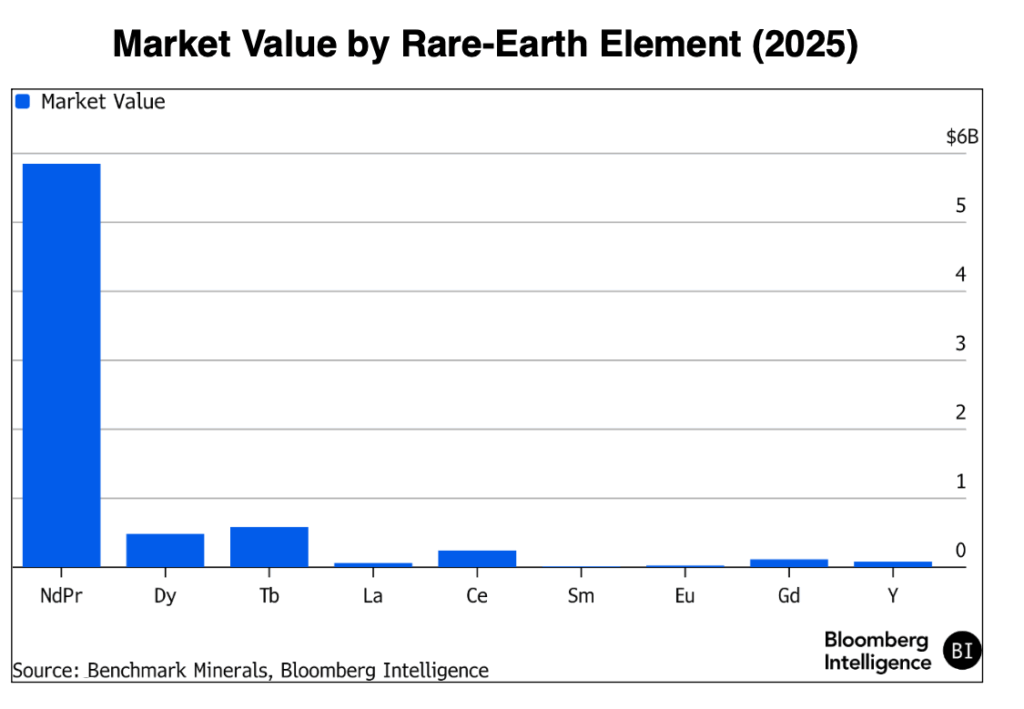

US-based MP Materials (NYSE: MP) and Australia’s Lynas Rare Earths (ASX: LYC) remain the leading producers of neodymium-praseodymium (NdPr), a crucial rare earth element used in heavy-duty magnets, outside China and stand to benefit as buyers seek secure sources of magnet-critical material. They are likely to ramp up output thanks to a raft of public funding from governments including the Trump administration, according to the report.

In the near term, however, Chinese incumbents such as China Northern Rare Earth and China Rare Earth Group are likely to capture higher prices as tightening conditions lift commodity markets.

NdPr production outside China is forecast to increase 4.4 times between 2024 and 2030, led by mines in North America and Australia, but much of that supply is already committed and will fall short of demand from vehicle manufacturers, electronics makers and defence contractors.

NdPr demand is projected to rise 7% annually through 2030, supported by technology and industrial growth, with companies such as Apple, BYD and Lockheed Martin collectively relying on roughly 97,000 metric tons a year.

Rapid price shift

Pricing power is shifting quickly. Potential Chinese export quotas could displace as much as 13,000 metric tons of demand in 2026, forcing Japanese industry and Western defence suppliers to act as marginal buyers in a bifurcated market, the report shows.

Rare-earth permanent magnets remain favoured for military applications over heavier, less efficient substitutes, and NATO members’ commitments to increase defence spending have elevated supply-chain security to a strategic priority.

Rare-earth equities have re-rated sharply since 2025, though performance varies by region and exposure. Chinese producers have rallied alongside commodity prices, gains that may prove temporary as governments pursue coordinated strategies to reduce reliance on Chinese supply.

Outside China, capital has concentrated in established players such as MP Materials and Lynas, where government partnerships are lowering project and earnings risk.

Meanwhile, magnet-manufacturing expansion in the US, Europe and Japan is being driven largely by mid-cap and private firms backed by concessional debt and policy incentives tied to execution.

As the US and its allies combine funding, mine development and industrial expertise, rare-earth markets are moving beyond traditional cyclical drivers toward a more protectionist and strategically aligned pricing regime, with sustained volatility likely as supply struggles to catch up.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments