War squeezes global mining as diesel and acid supplies tighten

From the Australian outback to Ethiopia and the Democratic Republic of Congo, the global mining industry is beginning to feel the effects of disruption caused by the war in Iran.

War-driven snarl-ups are starting to ripple through supply chains, squeezing access to key mining inputs while driving up costs to produce some of the world’s most sought-after metals. The biggest impacts are from diesel, the main fuel powering heavy equipment at mine sites, as well as sulfur, used in processing about a sixth of the world’s copper.

“The supply chain is breaking down,” Ivanhoe Mines Ltd. founder and co-chairman Robert Friedland told a conference in Switzerland Tuesday, warning that war’s impact on mining has barely started.

So far, there hasn’t been a significant impact on global metals output because big mining companies have been able to secure supplies and absorb higher costs. But smaller producers from Africa to Australia are starting to feel the pain as the conflict drags on. The longer the war continues, the greater the risks to an industry already strained by mining outages and project delays at a time of accelerating demand for critical minerals.

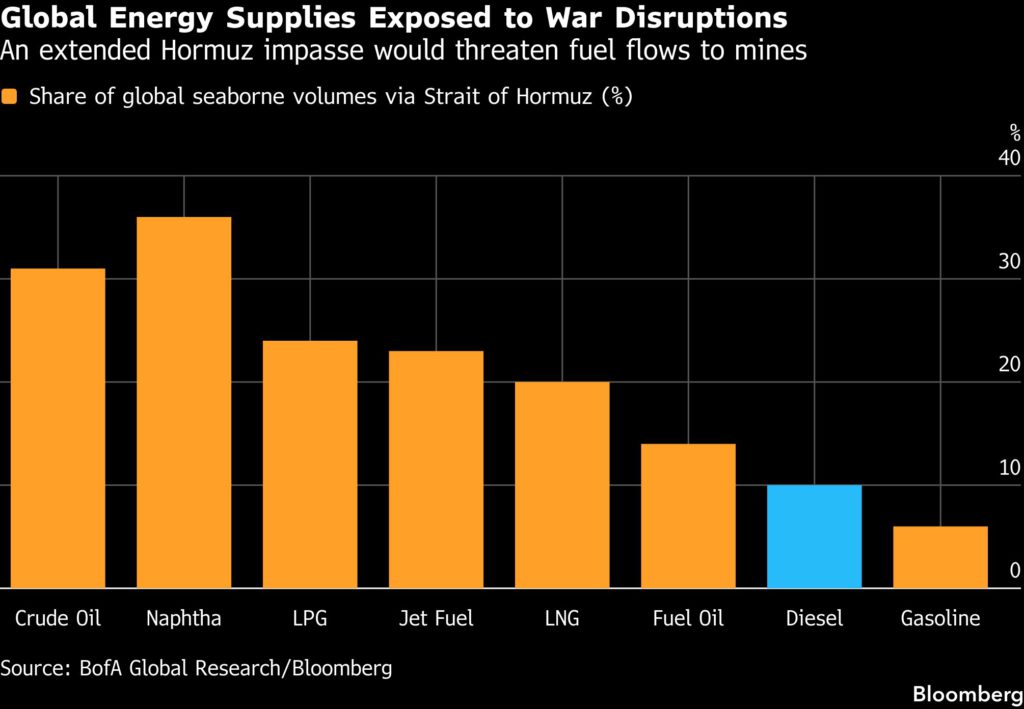

The Middle East accounts for about half the world’s seaborne sulfur and at least 10% of shipped diesel, according to data compiled by Goldman Sachs Group and Bank of America. Sulfur — and by extension, sulfuric acid — are vital inputs for a type of processing known as SX-EW, which accounts for 17% of copper supply, according to Goldman.

If war-related upheavals intensify, it could start eroding the 23 million tons of copper mined per year in a more meaningful way and drive up already elevated metal prices even more. Futures on the London Metal Exchange are more than 40% higher than a year ago, and in January touched a record high above $14,500 a ton.

Congo — the world’s No. 2 copper producer and biggest supplier of cobalt, a battery metal — is particularly exposed because most of its sulfur comes from the Middle East and its output is unusually reliant on SX-EW plants. SX-EW uses acid to leach copper and cobalt out of certain types of ore, without needing smelters that actually generate acid as a byproduct.

Securing new sulfur supply could take almost two months while inventories at some facilities cover only a month, according to a person with knowledge of the situation. Some smaller cobalt and copper operators are slowing output amid difficulties getting affordable sulfur and spiking diesel costs, said the person.

Local sulfur prices have surged to about $1,200 a ton, about double from before the Iran war, according to pricing agency Argus. Some local buyers said smaller parcels even reached $1,400 a ton as copper plants are eager to stock up.

If supply chain delays extend through June, Goldman analysts estimate the Central African nation could curtail about 125,000 tons of output this year.

In Zambia, a combination of disrupted supply from local smelters and the Middle East war means “sulfuric acid is a worry,” said Jonathan Morley-Kirk, finance director at Jubilee Metals Group Plc. The copper company has explored pooling purchases with other operators, he said on a recent earnings call.

Mining executives may offer a clearer read on disruption threats in the coming weeks as companies report quarterly results.

Adding to the Middle East’s sulfur disruptions, China has signaled plans to halt exports from May of acid produced as a byproduct of copper and zinc smelting. Beijing’s curbs could remove about 1.5 million tons of acid through December, or roughly a tenth of the seaborne market, according to Goldman.

That poses a particular challenge for Chile, which sourced about 30% of its acid from China last year. If restrictions hold through year-end, as much as 200,000 tons of acid-dependent metal output would be put at risk in the top copper-producing nation — or about 1% of global supply, Goldman analysts wrote in an April 21 note.

To be sure, Chilean copper giant Codelco produces most of the acid it consumes and locked in prices before the war, though it is closely monitoring suppliers’ ability to deliver, chief commercial officer Braim Chiple said. US copper producer Freeport-McMoRan Inc. is similarly hedged, though chief executive officer Kathleen Quirk said in an interview that acid supply is “on the list of things to worry about.”

While sulfur markets are tightening, traders say buyers are still able to secure alternative cargoes.

“The sulfur is there for those who can pay the price,” Graeme Train, Trafigura’s global head of metals and minerals analysis, said Monday at the FT Commodities Global Summit.

Some nickel producers in Indonesia have sourced sulfur from Central Asia and Canada, albeit at sharply higher prices, said a person familiar with the situation.

China’s Zhejiang Huayou Cobalt Co. said it doesn’t rule out cutting output if sulfur supply remains tight. The company, which uses sulfur at some of its Indonesian nickel plants, was “caught off guard” after prices surged, chairman Chen Xuehua said on a Monday earnings call.

In Australia, Lynas Rare Earths Ltd. is confident it can get enough sulfuric acid for its domestic processing plants and Malaysian refinery, but the big effect is prices, CEO Amanda Lacaze said on a Monday investor briefing. “We expect that sulfuric acid alongside some other transport cost increases, etc., will make it a little more challenging for us in terms of costs” this quarter.

Diesel disruptions are also pushing up mining costs, particularly for open-pit operations in copper, coal, iron ore and hard-rock lithium. Major producers such as Codelco and Antofagasta Plc estimate the impact at about a 5% increase in production costs — manageable given strong margins.

The bigger risk in some regions is physical availability. Congo again stands out, as copper-cobalt mines rely on imported diesel hauled across long, complex supply routes.

“This fragmented and logistics-intensive supply chain makes diesel availability particularly constrained and costly in mining regions,” BofA analysts wrote in an April 17 note. “Fuel availability in the DRC is not merely a cost variable, but a critical operational constraint.”

Global fuel upheavals tightened diesel availability in Ethiopia, according to Akobo Minerals AB, prompting the Oslo-listed firm to temporarily scale back operations at its Segele project.

In Australia, diesel shortages have already affected some smaller miners, while major producers remain largely insulated: Rio Tinto Group said in its latest production report that operational impacts have been limited, though rising fuel prices are lifting costs.

Fuel constraints forced iron ore producer Fenix Resources Ltd. to curtail activity, reducing non-essential mining and haulage at its Western Australia operations, the company said last month. There are reports of difficulties in booking Indonesian coal shipments after June because of concerns over securing diesel supplies.

Some of the world’s largest mining companies, with operations from Southeast Asia to Latin America, are starting to warn investors of rising costs tied to the Middle East conflict.

Teck Resources Ltd. warned of higher fuel costs for its flagship Chilean copper mines Thursday in its earnings report. While the Vancouver-based company said it didn’t see a significant risk to fuel supply disruption, “there could be an amplified impact on costs at our Chilean operation due to the requirement for diesel imports.”

Freeport, which operates the massive Grasberg copper mine in Indonesia, lifted its 2026 cost estimates in part because prices for diesel and sulfuric acid have been highly volatile with significant regional dislocation.

The chairman of Chile’s state-owned Codelco, Maximo Pacheco, said the war’s impacts have become an unexpected headwind for the industry.

“Nobody expected this to happen,” he said in an interview. “Producing copper today is more and more difficult.”

Read More: Chinese copper output hits record on tailwind from sulfuric acid

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments