Top 50 mining companies reshuffle as Chinese, lithium firms climb rankings

Tintaya concentrator Peru. Source: Glencore

After a banner 2016, the recovery in the mining sector slowed dramatically this year and in some instances fortunes reversed.

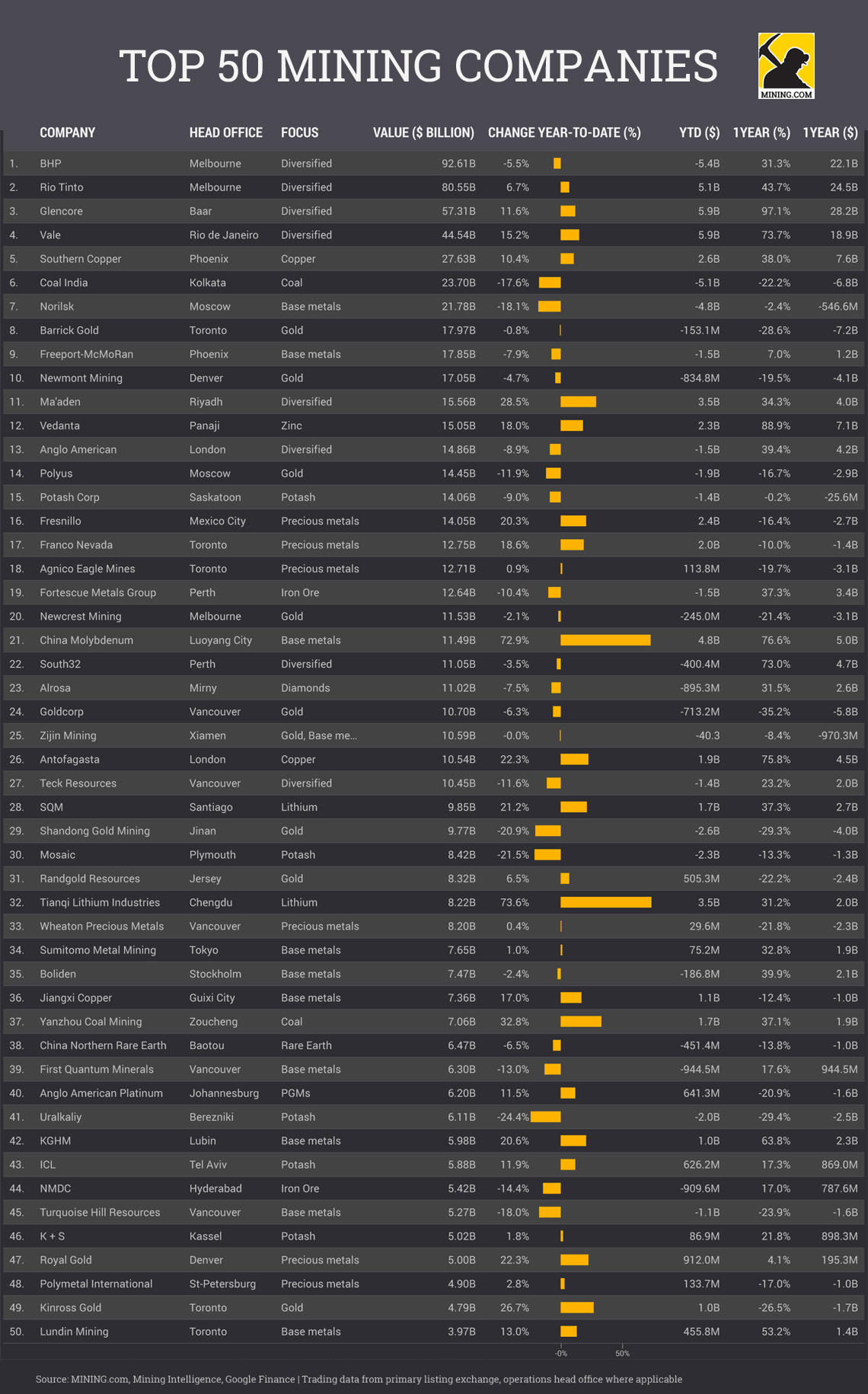

At the half-year mark, the world’s 50 largest listed firms are worth a collective $768 billion, adding nearly $12 billion in market capitalization to year-to-end June. The top 10 make up more than half the sector’s worth.

The vast majority of those gains were achieved last year – over the past 12 months the top 50 have added nearly $100 billion in combined value.

A handful of gold companies are in the red so far this year, notably China’s Shandong Gold, Canada’s Goldcorp and Russia’s Polyus Gold, the world’s eighth largest gold miner. Some of last year’s high flyers have also come back down to earth including Australia’s Fortescue Metals Group which have been declining alongside the iron ore price and Canada’s Teck Resources, hurt by a coking coal price that’s fallen back to earth.

Perth-based Iluka Resources is also in contention after jumping 20% in market value this year at $2.8 billion which would make it the sole mineral sands miner in the top 50

Russian firms are not having a happy 2017 with the top five companies losing $9.5 billion year-to-date as falling nickel prices hurt Norilsk’s prospects and potash prices languishing near multi-year lows crimp Uralkali’s outlook. In fact US-based Mosaic and Uralkali have fallen most in percentage terms in H1 2017 and Canada’s Potash Corp (to be known as Nutrien following merger with Agrium) just escaped double digit declines.

In contrast to middling performances from North American and Europe-based companies, three of the seven Chinese firms in the ranking are 2017’s top gainers. Tianqi Lithium continues to ride the battery raw material wave with a near 75% jump in value. China Molybdenum is also on a roll as is Yanzhou Coal with both companies making the most of their jump in value to go on the acquisition path outside their home base.

There has been a few notable changes in the ranking with India’s Vedanta making the most of the continued rally in zinc prices to overtake diversified giant Anglo American to take 12th spot. Saudi Arabia’s Ma’aden also continues to climb the ranking and is now knocking on the door of the top 10. After joining the top 50 last year Tanqui Lithium continued its ascent this year and now ranks as the 32nd most valuable mining company, catching up to another lithium darling Chile’s SQM.

Companies that could join or rejoin the ranking include Canada’s Cameco, the world’s number one public uranium miner which sits at no 51 with a market value of $3.7 billion, London-listed KAZ Minerals ($3.1 billion), Peru’s Buenaventura ($3 billion) and Ivanhoe Mines, a platinum and copper explorer which is up in nearly fourfold in value over the past year and now worth $2.4 billion. Australia’s Iluka Resources is also in contention after jumping 20% in market capitalization this year at $2.8 billion which would make it the sole mineral sands miner (with a bit of iron ore on the side) in the top 50.

Share data last reading on July 3 2017.

Notes:

As with any ranking, criteria for inclusion is a contentious issue. We decided to exclude unlisted and state-owned enterprises at the outset due to a lack of information. That of course excludes giants like Chile’s Codelco, Uzbekistan’s Navoi Mining which owns the world’s largest gold mine, Eurochem, a major potash firm, trader Trafigura, top uranium producer Kazatomprom and numerous entities in China and developing countries around the world.

Another central criterion was the depth of involvement in the industry before an enterprise can rightfully be called a mining company.

For instance, should smelter companies or commodity traders that own minority stakes in mining assets be included, especially if these investments have no operational component or not even warrant a seat on the board?

This is a common structure in Asia and excluding these types of companies removed well-known names like Japan’s Marubeni and Mitsui, Korea Zinc and Chile’s Copec.

Levels of operational involvement and size of shareholding was another central consideration. Do streaming and royalty companies that receive metals from mining operations without shareholding qualify or is are they just specialized financing vehicles? We included Franco Nevada and Silver Wheaton (now Wheaton Precious Metals).

What about diversified companies such as BHP Billiton or Teck with substantial oil and gas assets? Or oil sands companies that use conventional mining methods to extract bitumen for that matter?

Vertically integrated concerns like Alcoa and energy companies such as Shenhua Energy where power, ports and railways make up a large portion of revenues pose a problem as does diversified companies such as Anglo American with separately listed majority owned subsidiaries. We’ve included Angloplat in the ranking, but excluded Kumba Iron Ore, which does not include Anglo’s Brazilian iron ore assets.

Chemical companies are also problematic – should FMC Corp not be ranked because its potash and lithium operations are such a small part of its overall revenues and what about Albermarle? While the merger of Potash Corp and Agrium is still to close we included only Potash Corp on this listing.

Many steelmakers own and often operate iron ore and other metal mines, but in the interest of balance and diversity we excluded the steel industry, and with that many companies that have substantial mining assets including giants like ArcelorMittal, Magnitogorsk, Ternium, Baosteel and many others.

Head office refers to operational headquarters wherever applicable. Trading data from primary listing exchange.

Please let us know of any omissions, deletions or additions to the ranking or suggest a different methodology.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

2 Comments

Howard Spiegel

Please advise where the $value comes from. The market capitalization is very different than these numbers.

BSN

What about Shenhua? Largest coal miner in the world – market cap >$60bn today, so should be 3rd in your list.