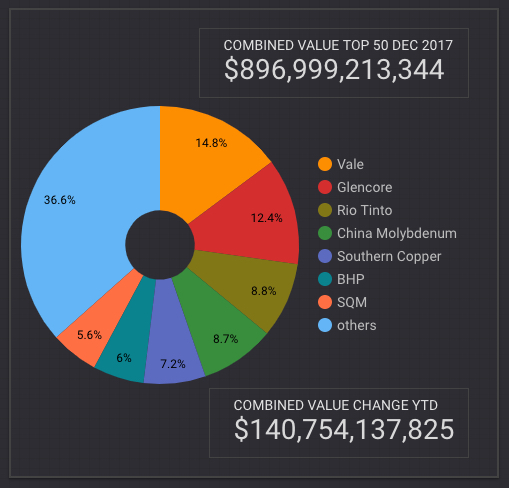

Value of top 50 mining companies surge $140 billion in 2017

Heading into 2018 the world’s 50 largest listed firms are worth a collective $896 billion, adding $141 billion in combined market capitalization year-to-date, with the bulk of those gains recorded since July.

Go back to the start of the mining industry’s upswing around 18 months ago and $227 billion of wealth has been created for shareholders of the MINING.com Top 50.

The top 10 make up more than half the sector’s market value and after underperforming the rest of the field during the first half of 2017, the big diversified and base metals companies caught up rapidly.

Of the gains since end-June nearly 65% have accrued to the top 10 largest mining companies. Year-to-date just two companies – Vale and Glencore – constitute 27% of market capitalization growth.

Gold companies have had a tough go of it this year with top producers Newmont Mining and Barrick Gold falling out of the top 10. Newmont overtook Barrick as the world’s most valuable gold miner this year, but was pushed out of the top tier by diversified giant Anglo American which continues to climb the rankings after years in the wilderness.

New entrant to the top 10 is high-flying China Molybdenum, the best performing mining stock in the world this year with a 150% gain in value year-to-date. The company started the year in 31st spot. The Luoyang City-based base metal giant is now worth more than $20 billion (also the bar for admittance to the top ten) as its acquisition spree of recent years begins to pay off in a big way.

Another company making the most of the rally in copper and zinc this year is KAZ Minerals which joins the Top 50 for the first time. The Kazakh company is up 120% in 2017 and worth $4.7 billion. At the beginning of 2017 a market value of less than $4 billion was enough for entry into the MINING.com Top 50.

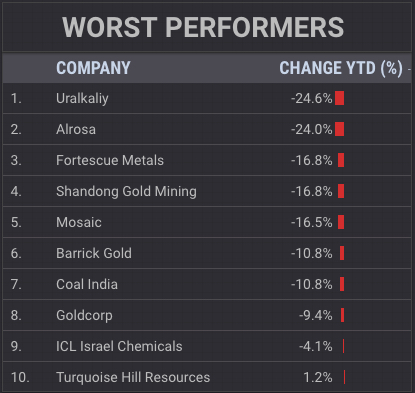

Only nine out of 50 firms are trading in negative territory for 2017 with Russian operations and potash proving a deadly combination. Russian diamond miner Alrosa has had a dismal year suffering a similar fall as that of Uralkaliy, the worst performing mining stock this year. The potash producer’s 24% decline drops the company from position number 30 at the start of the year down to a 44 ranking.

Dropping out of the Top 50 is German-based potash miner K+S after losing over 10% of its value in 2017. Of the four remaining fertilizer miners in the Top 50, Potashcorp of Saskatchewan bucked the weaker trend with an 8.4% gain this year as it looks to close the merger with US-based Agrium to create the world’s largest producer of the crop nutrient.

Fullscreen available. Scroll down for full ranking, country data (drop down menu). Stock exchange and currency cross rates last reading December 19, 2017. See notes below for more information and selection criteria.

Notes:

As with any ranking, criteria for inclusion is a contentious issue. We decided to exclude unlisted and state-owned enterprises at the outset due to a lack of information. That of course excludes giants like Chile’s Codelco, Uzbekistan’s Navoi Mining which owns the world’s largest gold mine, Eurochem, a major potash firm, trader Trafigura, top uranium producer Kazatomprom and numerous entities in China and developing countries around the world.

Another central criterion was the depth of involvement in the industry before an enterprise can rightfully be called a mining company.

For instance, should smelter companies or commodity traders that own minority stakes in mining assets be included, especially if these investments have no operational component or not even warrant a seat on the board?

This is a common structure in Asia and excluding these types of companies removed well-known names like Japan’s Marubeni and Mitsui, Korea Zinc and Chile’s Copec. Levels of operational involvement and size of shareholding was another central consideration. Do streaming and royalty companies that receive metals from mining operations without shareholding qualify or is are they just specialized financing vehicles? We included Franco Nevada and Silver Wheaton (now Wheaton Precious Metals).

What about diversified companies such as BHP Billiton or Teck with substantial oil and gas assets? Or oil sands companies that use conventional mining methods to extract bitumen for that matter? Vertically integrated concerns like Alcoa and energy companies such as Shenhua Energy where power, ports and railways make up a large portion of revenues pose a problem as does diversified companies such as Anglo American with separately listed majority owned subsidiaries. We’ve included Angloplat in the ranking as well as Kumba Iron Ore.

Chemical companies are also problematic – should FMC Corp not be ranked because its potash and lithium operations are such a small part of its overall revenues and what about Albermarle? While the merger of Potash Corp and Agrium is still to close we included only Potash Corp on this listing.

Many steelmakers own and often operate iron ore and other metal mines, but in the interest of balance and diversity we excluded the steel industry, and with that many companies that have substantial mining assets including giants like ArcelorMittal, Magnitogorsk, Ternium, Baosteel and many others.

Head office refers to operational headquarters wherever applicable, for example BHP and Rio Tinto is shown as Melbourne, Australia and Antofagasta is grouped with Chile even though the company is HQ’ed in London where it has been listed since the late 1800s. Trading data from primary listing exchange and currency cross-rates at the date of publication.

Please let us know of any omissions, deletions or additions to the ranking or suggest a different methodology.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

2 Comments

Weiping Liu

Hi, how do you calculate the market capitalization value? Is it from the company 2017 annual report? Or you just sum the result of the price multiplying outstanding share in different exchange? I am doing research related to your paper right now. I may need to cite your data, so I want to know the logic behind those number. Thanks!

MINING.com Editors

The latter. The market capitalization data is from the various exchanges the companies are listed on incl TSX, ASX, HKG, Shanghai, LSE, MCX, Bovespa. Last share price, shares outstanding and currency exchange rates data as at 20 Dec 2017 via Googlefinance. There are different opinions on how to calculate market cap using free float only – see this discussion at the bottom of a previous post: http://bit.ly/2tiACeI. I’d be interest in reading your research report. – Frik