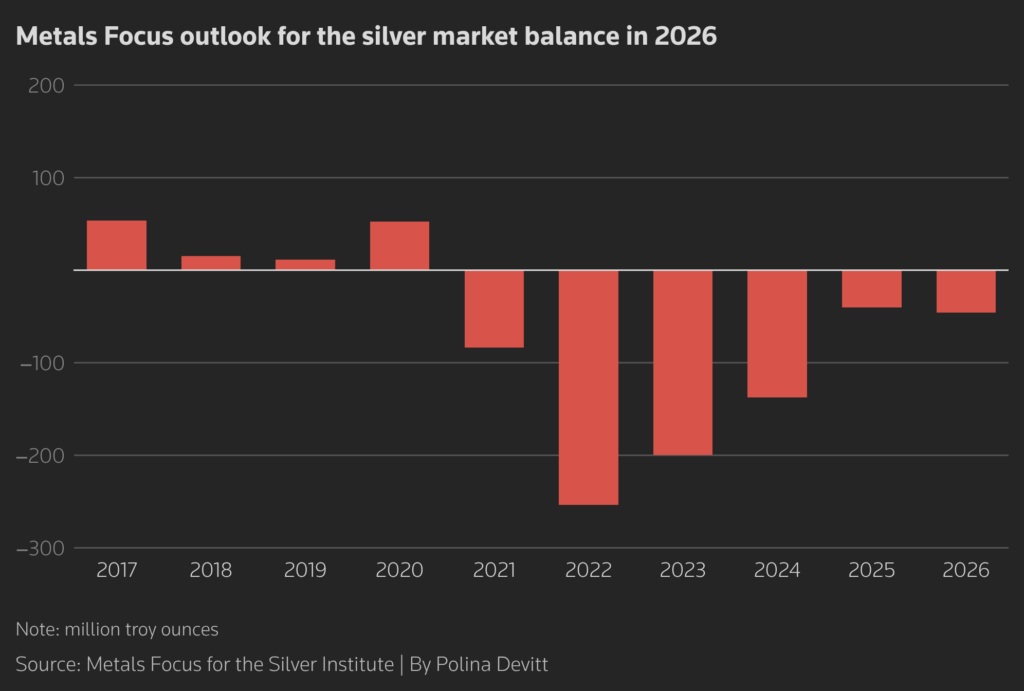

Silver faces sixth year of deficit with stock drawdown raising squeeze risks, research shows

The silver market is heading for a sixth year of structural deficit, with 762 million troy ounces drawn from stocks since 2021, raising the risk of a renewed liquidity squeeze despite weaker demand expectations, the Silver Institute and consultancy Metals Focus said on Wednesday.

Silver , used in jewellery, electronics, electric vehicles and solar panels as well as for investment, is down 35% since a bout of frenzied retail buying – following a 147% surge in 2025 – drove prices to a record high of $121.6 an ounce in January.

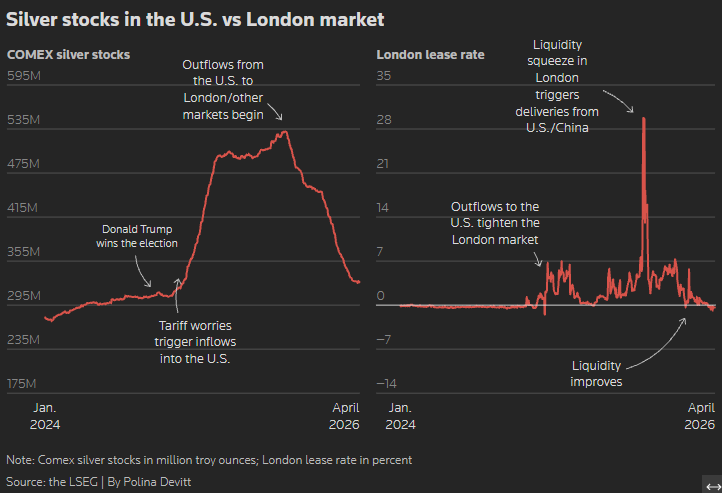

The base for that rally was created in 2025 by months of inflows of the metal to the US inventories and silver-backed exchange-traded products (ETPs) alongside a spike in physical demand that triggered a liquidity squeeze in the benchmark London market in October.

Since then, liquidity has improved as metal flowed back from the US, ETPs saw outflows and Indian demand eased.

“Lease rates in London have largely normalized, but risks of another liquidity squeeze this year remain,” said Philip Newman, managing director at Metals Focus, which prepared the research for the Silver Institute industry association.

Metals Focus estimates that 28% of 884 million ounces of silver held in London vaults at end-March were not tied to ETPs and were potentially available to support liquidity, the highest share since January 2025 and up from a historic low of 17% in September that helped precipitate the October squeeze.

Conditions for a silver squeeze will be created again, requiring further outflows from the US, if the price becomes more volatile and Indian demand gets active, especially coupled with inflows to ETPs storing their metal in London, Newman said.

The global silver market deficit is expected to widen to 46.3 million ounces in 2026 from 40.3 million in 2025, even as total demand falls 2% due to weaker industrial and jewellery consumption, partly offset by stronger coin and bar demand, the research showed.

Industrial silver fabrication is forecast to fall 3% to a four-year low with the Iran war’s damage to global growth threatening further downside. By contrast, coin and bar demand is seen rising 18% supported by a recovery in the US buying.

Total global silver supply is forecast to decline 2%, reflecting producer hedging normalizing after jumping in the second half of 2025.

(By Polina Devitt; Editing by Joe Bavier)

More News

Bomb attack damages Ecuador mining agency probing illegal gold

It’s the second blast in recent weeks affecting Arcom offices.

June 29, 2026 | 12:28 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments