Cobalt price rally boosts MINING.COM EV Metal Index

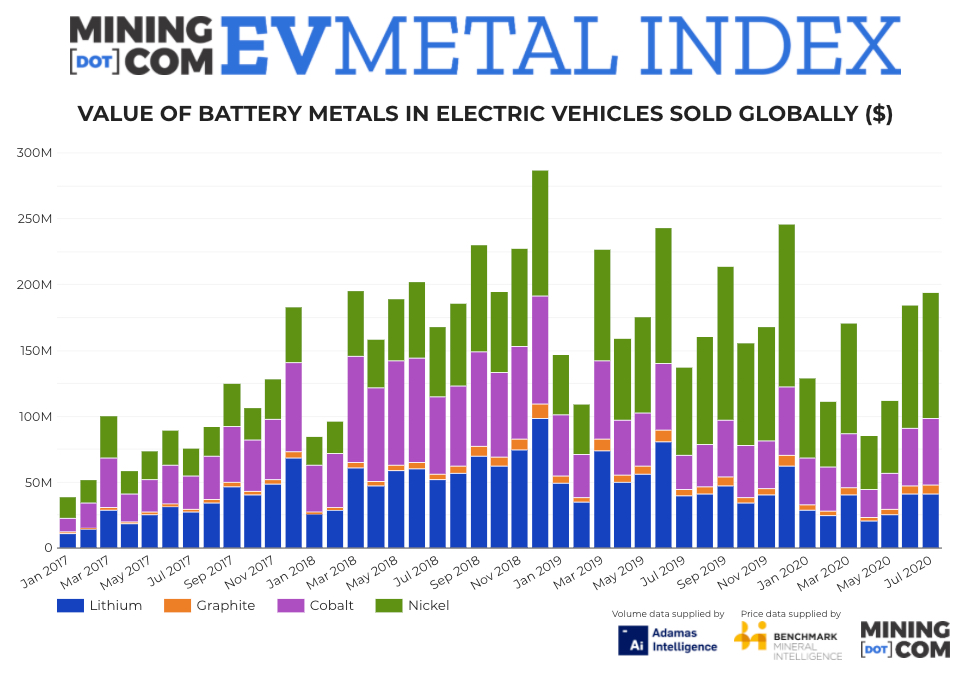

The MINING.COM EV Metal Index, which tracks the value of battery metals in newly registered passenger EVs (including plug-in hybrids) around the world continued to recover month on month in July, after dropping to its lowest level since January 2018 in April.

A modest uptick in raw material deployed (with the exception of nickel) and a sharp year-to-date rally in cobalt, combined with improving prices for nickel used in the supply chain lifted the value of battery raw materials tracked by the index to $194 million for the month.

“The link between all of these recent cobalt stockpiling efforts is that the purchases were all taken in a low-price environment, as such this could mark a point where cobalt prices begin a sustained rise”

Benchmark Mineral Intelligence

At $988 million year-to-date, the index is still more than 17% below 2019 levels although, as testament to the youth of the electric vehicle market, is double the value of the same period in 2017.

SRB could give cobalt another leg up

An 8.6% jump in the price of cobalt combined with a double-digit increase in deployed cobalt lifted the sub-index to above $50 million for the first time this year.

Cobalt prices have been underpinned this year due to tight supply resulting from export restriction earlier in the year of cobalt from the DRC shipped through South Africa and expectations that top cobalt miner Glencore will keep its Mutanda mine – responsible for 20% of global output – on care and maintenance for at least another couple of years.

Rumours that China’s State Reserve Bureau (SRB) is undertaking significant purchases of cobalt to stockpile the country’s strategic reserves have now been confirmed, further chasing up the price.

Benchmark Mineral Intelligence is anticipating a minimum of 2,000 tonnes of cobalt metal to be purchased by the SRB, with an upper range of 5,000 tonnes.

Annual cobalt production is only around 130,000 tonnes, mostly as a byproduct of nickel and copper mining. Of that, roughly 30,000 tonnes is in metal form which makes even just 2,000 tonnes a significant market mover.

The SRB made similar purchases in 2014–2016, says Benchmark:

“The link between all of these recent cobalt stockpiling efforts is that the purchases were all taken in a low-price environment, as such this could mark a point where cobalt prices begin a sustained rise.”

Lithium price declines continue

Lithium and graphite prices eased again in July, albeit slightly, with the former falling below $7,000 a tonne for the first time since September 2015, according to Benchmark Mineral Intelligence data.

Nickel sulphate index prices climbed back above $15,000 a tonne (100% Ni basis), but deployment weakened compared to June to just above 6,300 tonnes, according to Adamas Intelligence data.

Europe holds EV lead

Europe is (just) keeping ahead of China – not long ago responsible for every other electric car sold worldwide – as the globe’s largest EV market.

Europe’s electric vehicle sales (including plug-in hybrids) outpaced those of China, reaching 597,700 units for the January–August period. That is already more than the 546,000 units sold all of last year.

Europe also held onto the lead despite a record-breaking August with sales of 109,000 units, up nearly 26% from the last year. Chinese so-called New Energy Vehicle (NEV) sales data also include fuel cell and commercial vehicles.

China still leads the charge in full battery electric vehicles, however. According to Schmidt, a market researcher, for the year to end-July of this year, 317,800 BEVs were sold in Western Europe compared to 466,000 in China.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments