Column: Study group shines some light on Doctor Copper’s confusion

(The opinions expressed here are those of Andy Home, a columnist for Reuters.)

Where next for Doctor Copper?

After January’s frenzied rush to record highs, the copper market is now nervously treading water, bobbing to the ever-changing news flow around the Iran crisis.

The closure of the Strait of Hormuz is both bullish and bearish for the copper price.

The Gulf is a major exporter of sulphur and copper miners using leaching technology need a lot of sulphuric acid. Solvent extraction and electrowinning accounts for a quarter of global refined metal output.

But the broader economic fallout from higher energy prices threatens a slowdown in manufacturing activity and therefore copper demand. It’s a risk that grows with each day the Strait remains closed.

The Iran crisis accentuates the confused and confusing play of opposing forces in the copper price.

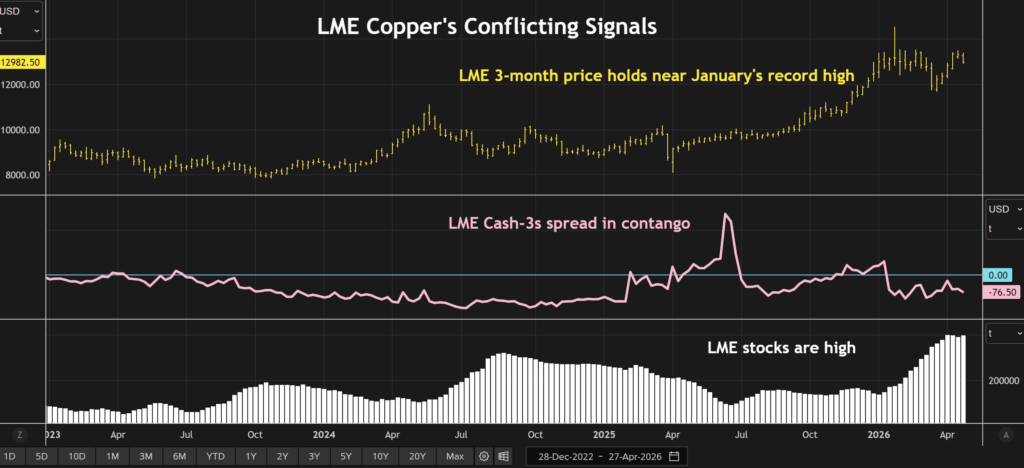

Supply is problematic. So too is demand. At $13,000 per metric ton, London Metal Exchange three-month copper is pricing scarcity. Yet exchange warehouses are full of metal and time-spreads are in deep contango, signalling abundance.

The latest forecasts from the International Copper Study Group (ICSG) shed some welcome statistical light on Doctor Copper’s current dilemma.

Finely balanced

Copper’s fundamental outlook depends on which deteriorates faster – supply or demand.

Global mined production grew by just 0.9% in 2025 relative to 2024 after big production hits in Chile, Indonesia and the Democratic Republic of Congo.

The lingering impact of those incidents has caused the ICSG to revise downwards expected mine production growth this year to 1.6% from 2.3% when it last met in October.

The ongoing squeeze in the copper concentrates segment of the market, reflected in historically low smelter treatment charges, is expected to restrain refined metal production growth to just 0.4% this year.

So far, so bullish.

But the ICSG also cut its copper usage forecast for this year to 1.6% from October’s 2.1%, citing the Iran crisis, which is “likely to weaken the global economic outlook and negatively impact copper demand”.

The Group has flipped its 2026 market balance assessment from October’s anticipated shortfall of 150,000 metric tons to a small 96,000-ton supply surplus.

Relative to the 29 million tons of copper that will be used this year, this is a marginal change but one that captures copper’s fine balancing act between simultaneous risks on both supply and demand sides of the equation.

Glut in 2025

Last year was a completely different story, which helps explain why exchange inventory is so high.

The ICSG made some interesting revisions to its 2025 market assessments at April’s spring meeting.

The Group now calculates the global copper market recorded a significant supply surplus of 455,000 tons last year, more than double the 178,000-ton excess anticipated in October.

The revision reflects much higher-than-expected smelter production, both primary and secondary.

Global refined copper output grew by 4.5% last year relative to 2024. Back in October the anticipated growth rate was 3.4%. A year ago it was 2.9%.

The aggressive rate of increase has been led by China, which lifted output by 9%, equivalent to an extra million tons, in 2025, according to Macquarie Bank.

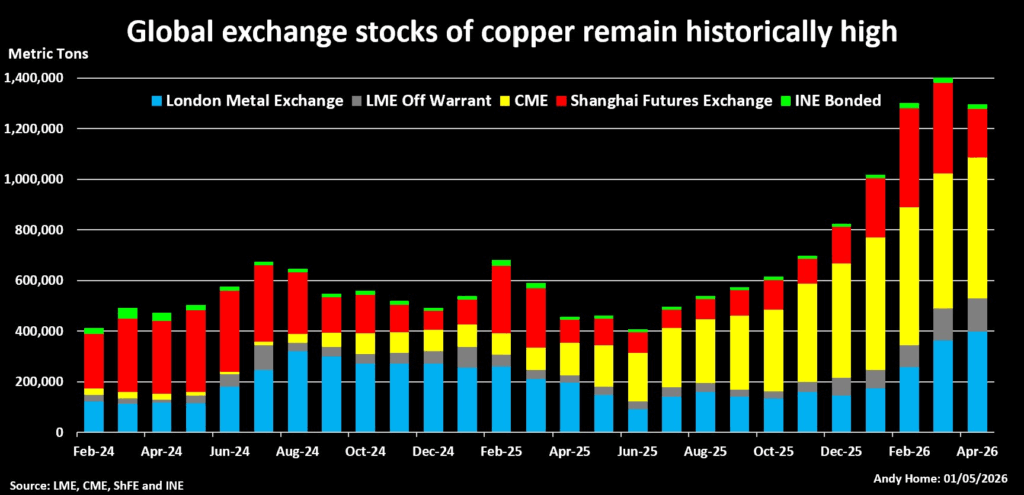

Much of last year’s surplus has been drawn to exchange warehouses, particularly those in the United States.

The US premium resulting from the threat of import tariffs on copper has sucked in copper from around the world and led to surging stocks at both CME’s domestic warehouses and LME warehouses in free trade zones.

Global exchange stocks of copper fell in April thanks to China’s post-holiday seasonal restock, but they remain historically high at 1.3 million tons, up by 800,000 tons since the start of last year.

Funds Trump fundamentals

Last year’s big supply surplus helps explain today’s high stocks and loose time-spreads.

On traditional metrics the price should be lower but it’s not because funds are currently trumping fundamentals.

The speculative buying frenzy of January has abated but there are plenty of investors keeping the bull faith in higher prices.

Money managers are net long to the tune of 59,132 contracts on the CME’s flagship contract, the largest bull commitment since the middle of January.

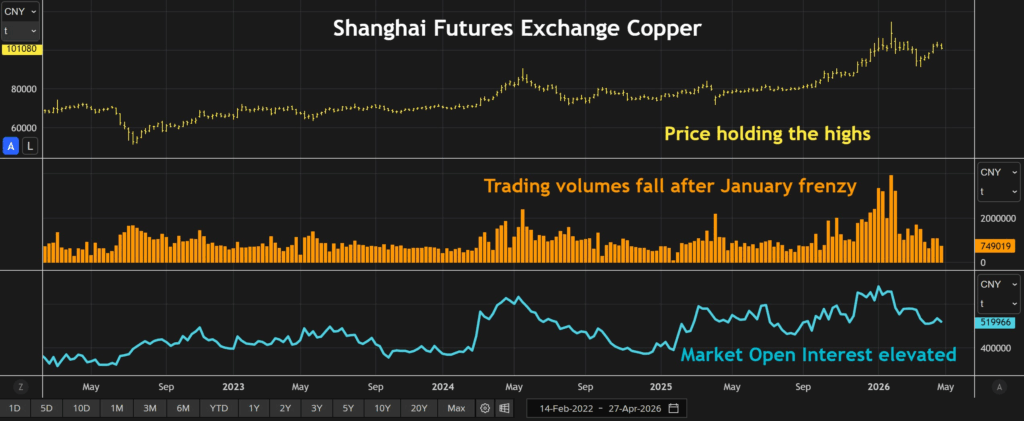

Market open interest on the Shanghai Futures Exchange copper contract, where the speculative fever was most intense, is still elevated at 520,000 contracts.

Copper’s fundamental dynamics are so nuanced right now that both bulls and bears can find plenty of fundamental ammunition to argue their respective cases.

But with investors holding the key, copper has become part of a multi-asset punt on the duration of the Iran war, which leaves both bulls and bears equally beholden to the next headline about the Strait of Hormuz.

(Editing by Kirsten Donovan)

More News

Bomb attack damages Ecuador mining agency probing illegal gold

It’s the second blast in recent weeks affecting Arcom offices.

June 29, 2026 | 12:28 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments