Top 50 mining companies power through Iran war – up $250 billion in 2026

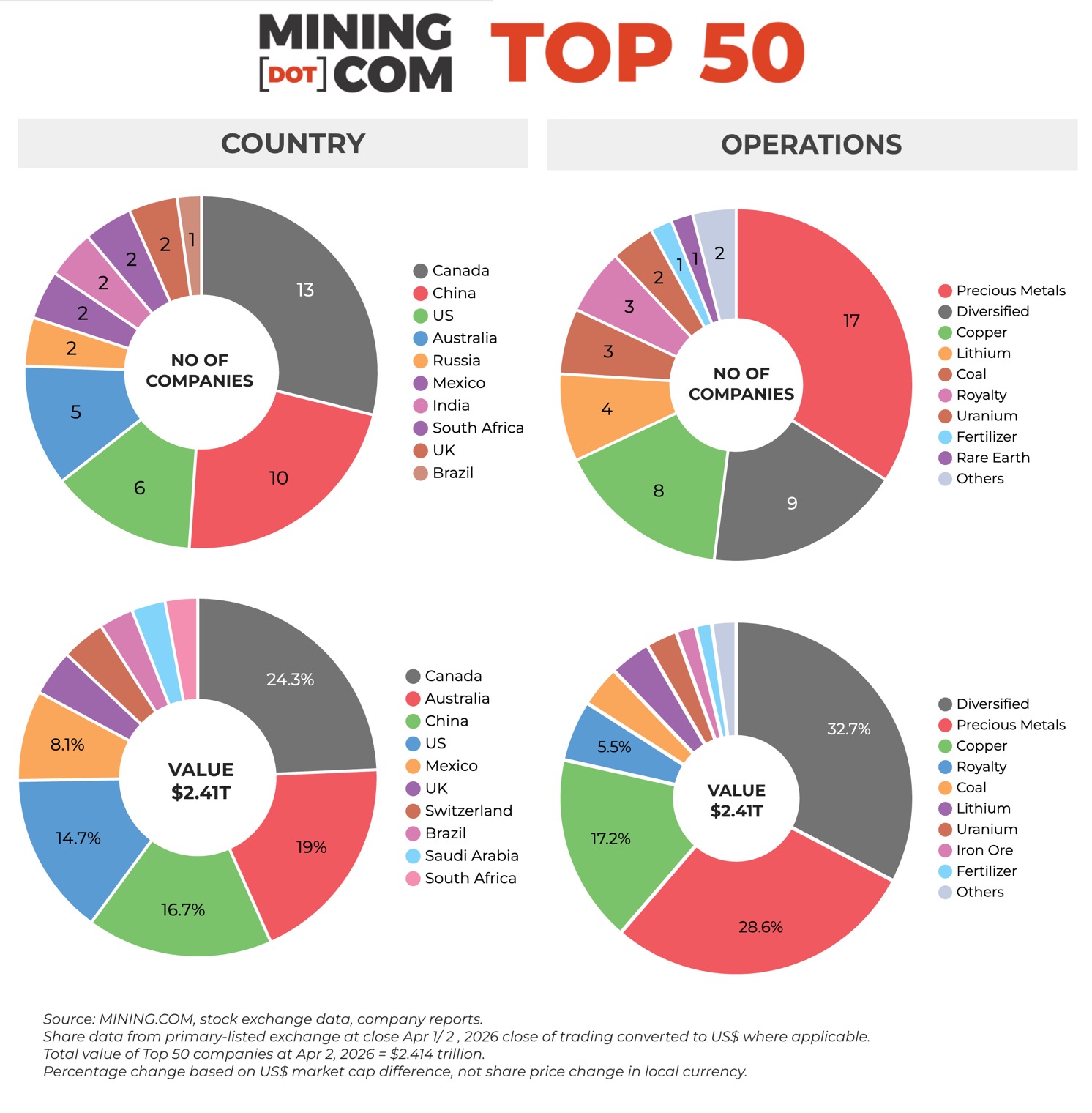

At the end of the first quarter the MINING.COM TOP 50* ranking of the world’s most valuable miners had a combined market capitalization of $2.41 trillion, up $250 billion so far in 2026.

The market correction for the world’s major miners and the metals that power them, came a full month before the start of the US-Iran war when gold and silver prices cratered after hitting record highs at the end of January. Stocks of precious metals producers and streamers tanked after gold dropped by double digits and silver entered freefall.

Gold has traded sideways since then, hovering above $4,700 an ounce and silver looks safe above $70 an ounce for now, although that’s still down 50% from its gravity defying spike. While gold did not receive the safe harbour investment a hot war in the Middle East would demand, the yellow metal is still showing a healthy 8% gain year to date. Silver is also trading in positive territory for 2026.

Copper is now down a modest 2% since end-2025 after hitting an all- time high of $6.50 per pound, or more than $14,000 the day before the Friday massacre, but at least one commodities trading desk is saying the bellwether metal is “oversupplied and overpriced” even after a $2,000 a tonne climbdown.

Lithium’s resurgence saw Chile’s SQM (NYSE:SQM) and US producer Albemarle (NYSE:ALB) return to the Top 50 in Q4 2025, bringing the number of lithium stocks in the Top 50 back to three (from the peak of six in 2022). The two companies together with China’s Ganfeng Lithium (SZSE:002460) also join the best performers list this quarter.

Mining’s majors have not exactly shrugged off the war, but measured from the start of 2026 most stocks are trending well into positive territory, with only a few exceptions.

Tide not lifting all boats

Among the upper echelons, Barrick Mining (NYSE:B) stands out with a 5% retreat year to date (versus Newmont’s (NYSE:NEM) 11% gain and Agnico Eagle’s 22% rise) as the company tries to unlock value from its portfolio by separately listing its North American gold assets and pursue a growth path in copper (hence the swap of gold for mining in the company name).

Barrick has assembled a new leadership team to run its US and Dominican Republic mines and last week tapped Goldman Sachs to lead the IPO, which by some estimates could value these assets at $60 billion on their own.

All things being equal, it values its risky operations in countries like military coup prone Mali, its Zambian copper assets and its massive Pakistan copper-gold project at only $10 billion at its current market cap. Things aren’t going well at Riko Diq and just last week Barrick warned of “significant increases” to the project’s budget and an extended timeline.

Another regular underperformer, Amman Minerals (IDX:AMMAN), tops the quarter’s worst list for the second time in a row with a 27% fall as production problems and delays at smelter commissioning in Indonesia (the country bans concentrate exports) takes the counter down another notch or two.

Amman was the first Indonesian company to make it into the top 50 after its blockbuster 2023 debut. After a fierce rally, the owner of the Batu Hijau copper and gold mine and developer of the adjacent Elang project even managed to pierce the top 10 briefly 18 months later, but it’s been downhill since.

Punter’s favourite Ivanhoe Mines (TSX:IVN) has lost almost a third of its value, and after dropping to a market worth below $11 billion at the end of Q1, no longer makes the grade for the Top 50, where the cut-off has risen to an $18 billion market capitalization.

Ivanhoe put its Kamoa-Kakula mine in the DRC into production mid-2021, the largest (and highest grade) copper mine to come online in decades. In 2024, the chairman of Zijin Mining, who owns 39.6% of the project and another 10% of Ivanhoe, said the company’s ambition is to make Kamoa-Kakula a 1 million tonne mine.

That dream has now receded into the distance. A year ago flooding at the mine led to temporary suspension of production and a nasty spat between Zijin and Ivanhoe and output has been slow to recover.

Just last week, Ivanhoe stunned investors eager for Ivanhoe to continue its DRC success story after slashing production guidance for 2026 to 290,000 to 330,000 tonnes, down from 380,000 to 420,000 tonnes. Next year will be even more disappointing: previously the company said it would produce as much as 540,000 tonnes, now the expectations are for 100,000 tonnes less.

The $100-billion club

Since inception, the MINING.COM TOP 50 was headed by two firms – BHP and Rio Tinto – the only miners with consistent market capitalizations above $100 billion (with a wobble here and there). Before 2025 the only other company to have that distinction was Vale (BOVESPA:VALE3) which for fleeting few days was also trading above this level during Q1 2022, the market’s previous peak.

Now there are six firms with the distinction. Agnico Eagle, (TSX:AEM) in January year entered the ranks of the triple digit billion dollar miner.

The Toronto-based company joined Chinese champion Zijin Mining (SHA: 601899), Southern Copper (NYSE: SCCO), the mining arm of Grupo Mexico, and Denver’s Newmont Corporation (NYSE: NEM) which rode gold and copper prices all the way to the top towards the end of last year.

BHP (ASX: BHP) managed to top $200 billion at the beginning of March, a distinction no other mining company has ever achieved (and for the second time – the first time was April 2022 although that lasted for a day). The Melbourne-based company released bumper profits in its half-year report with copper, including byproducts such as gold, contributing $7.95 billion to BHP’s operating earnings, topping iron ore for the first time.

BHP’s incoming CEO Brandon Craig, who takes the helm of the company at the end of May inherits a company balancing ambitious spending plans with investor expectations for returns after a period defined by bold — and not always successful — dealmaking, most notably its botched bid for Anglo American.

BHP and Rio Tinto (LSE: RIO) once again hold the two top spots. Rio Tinto was pushed out by Zijin and Southern Copper in January but the traditional order seems to have been restored, with some daylight between the Anglo-Australian giant and its competitors.

Rio Tinto stock received a lift after the company said on Monday it has gained control of acreage in Arizona needed to build the Resolution mine, a project slated to become one of the largest US sources of copper. Rio Tinto said it would now embark on a $500 million drilling campaign to delineate the deposit, which is co-owned by BHP.

Glencore, Freeport rebound

After being a perennial underperformer, Glencore (OTCPK: GLNCY) now has a better shot at joining the triple digit club. Glencore is now worth $87 billion and year to date the company is now the best performer among mining’s heavyweights with a 37% advance.

The Switzerland-headquartered company has escaped much of the fallout of US and Israeli operations in Iran in part to its extensive oil trading business which should do well as crude and gas prices jump, and a revival in coal.

The firm trades around 4 million barrels of oil equivalent per day. There was speculation last month from large investors in Glencore that a recent surge in coal prices will help bring Rio Tinto back to the table for a fresh attempt at creating the world’s biggest mining company after meeting with leaders of both companies in Australia.

Freeport McMoRan (NYSE: FCX) came within $1 billion of $100 billion towards the end of February after the stock rebounded from its September 2025 drop following a devastating mud-rush at the block cave underground operation in Indonesia.

Full production restart at Grasberg is predicted to happen at a quicker pace than early forecasts. Management targets restoring 85% of Grasberg’s production capacity by the second half of 2026. In February, Indonesia’s investment minister and Freeport’s unit in the Asian country signed a memorandum of understanding to extend the company’s mining permit for the iconic Grasberg mine beyond 2041.

It was reported in March that the Phoenix-based company has begun the environmental permitting process for a $7.5 billion expansion of its majority owned El Abra copper mine in Chile.

NOTES:

Source: MINING.COM, stock exchange data, company reports. Share data from primary-listed exchange on December 30, 2025 close of trading converted to US$ where applicable. Percentage change based on US$ market cap difference, not share price change in local currency.

As with any ranking, criteria for inclusion are contentious. We decided to exclude unlisted and state-owned enterprises at the outset due to a lack of information. That, of course, excludes giants like Chile’s Codelco, Uzbekistan’s Navoi Mining (the gold and uranium giant may list later this year), Eurochem, a major potash firm, and a number of entities in China and developing countries around the world.

Another central criterion was the depth of involvement in the industry, and how far upstream is the bulk of its revenue, before an enterprise can rightfully be called a mining company.

For instance, should smelter companies or commodity traders that own minority stakes in mining assets be included, especially if these investments have no operational component or even warrant a seat on the board? This is a common structure in Asia and excluding these types of companies removed well-known names like Japan’s Marubeni and Mitsui, Korea Zinc and Chile’s Copec.

Levels of operational or strategic involvement and size of shareholding were other central considerations. Do streaming and royalty companies that receive metals from mining operations without shareholding qualify or are they just specialized financing vehicles? We included Franco Nevada, Royal Gold and Wheaton Precious Metals on the basis of their deep involvement in the industry.

Vertically integrated concerns like Alcoa and energy companies such as Shenhua Energy or Bayan Resources where power, ports and railways make up a large portion of revenues pose a problem. The revenue mix also tends to change alongside volatile coal prices. Same goes for battery makers like China’s CATL which is increasingly moving upstream, but where mining will continue to represent a small portion of its valuation.

Another consideration is diversified companies such as Anglo American with separately listed majority-owned subsidiaries. We’ve included Angloplat (now Valterra) to track PGM representation in the ranking but excluded Kumba Iron Ore in which Anglo has a 70% stake to avoid double counting. Similarly, we excluded Hindustan Zinc which is listed separately but majority owned by Vedanta.

With other groups like Mexico’s Penoles where refining and chemicals make up a substantial part of the business where possible the Top 50 would include separately listed operating subsidiaries that are dedicated to mining. This is also why Southern Copper represents Grupo Mexico in the ranking.

Many steelmakers own and often operate iron ore and other metal mines, but in the interest of balance and diversity we excluded the steel industry, and with that many companies that have substantial mining assets including giants like ArcelorMittal, Magnitogorsk, Ternium, Baosteel and many others.

Head office refers to operational headquarters wherever applicable, for example BHP and Rio Tinto are shown as Melbourne, Australia, but Antofagasta is the exception that proves the rule. We consider the company’s HQ to be in London, where it has been listed since the late 1800s.

Please let us know of any errors, omissions, deletions or additions to the ranking or suggest a different methodology: email Frik Els at fels@mining.com with Top 50 in the subject line.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments